Alternative fuels challenge the sustainability of maritime decarbonisation

It is undisputable that we need to drive a lower carbon future. But how can we best achieve this with the resources we have at hand? In this article Kenneth Tveter, Head of Clarksons Green Transition team provides his views.

There are plenty of opinions about future fuels and the righteous path for our industry. The fuel discussion has similar characteristics to that of religion where you take a view and defend it with everything you have. With the Clarksons Green Transition team we have an agnostic approach based on facts and not vision. We are without biased towards one fuel over the other and only seek the most sustainable solution for our clients.

Sustainability and decarbonisation are two concepts that are often used in the same breath. However, in the maritime industry, they can be contradictory if the wrong approach to shipping fuel is taken.

Ignoring transition fuels such as LNG in favour of investment-heavy alternative fuels could be detrimental to the broader sustainability of our industry.

Alternative fuels are not the solution for here and now

In order to significantly cut greenhouse gases (GHGs), the shipping industry needs to move towards lower carbon fuels and we are, undoubtedly, moving from fossil-based fuels towards renewable electricity-based fuels (e-fuels) in the future. However, this future is not near and before we reach Utopia, we will be in a transition window with suboptimal solutions.

While we do we recognise the importance of early adopters of the of hydrogen-based fuels such as ammonia and methanol for the development of propulsion technology and infrastructure, we need to recognise the challenges with the production methods to meet conventional demand before we increase the production volumes to meet new demand from shipping.

Hydrogen as an alternative propulsion fuel

Looking at hydrogen first, around 94 million tons is currently being produced globally. However, current production of hydrogen is fossil and has an emissions profile equal to shipping, at around 900 million tonnes of CO2 per year. We need to first decarbonise production before we start thinking about increasing its supply.

About 1/3 of global hydrogen demand comes from the production of ammonia, a product that is essential for our survival. In order to justify the usage of ammonia and methanol as a maritime fuel, we would first need to decarbonise current production and secondly significantly increase production to meet new demand from shipping. Due to the nature and scale of the maritime industry, dedicating such a large volume of renewable energy towards fuel production would be no mean feat.

A significant part of the challenge when making shipping fuels from renewable energy is the energy losses in production and conversion.

When using 100 units of renewable energy to produce e-fuels, output at the propeller stands at just 25 units which is not sustainable compared to alternative applications in today’s era of limited renewable energy sources. We need to wait for renewable energy capacity to increase, and hopefully conversion efficiencies to further improve, before we can allow shipping at scale to join the race for alternative fuels if we seek a sustainable path towards decarbonisation.

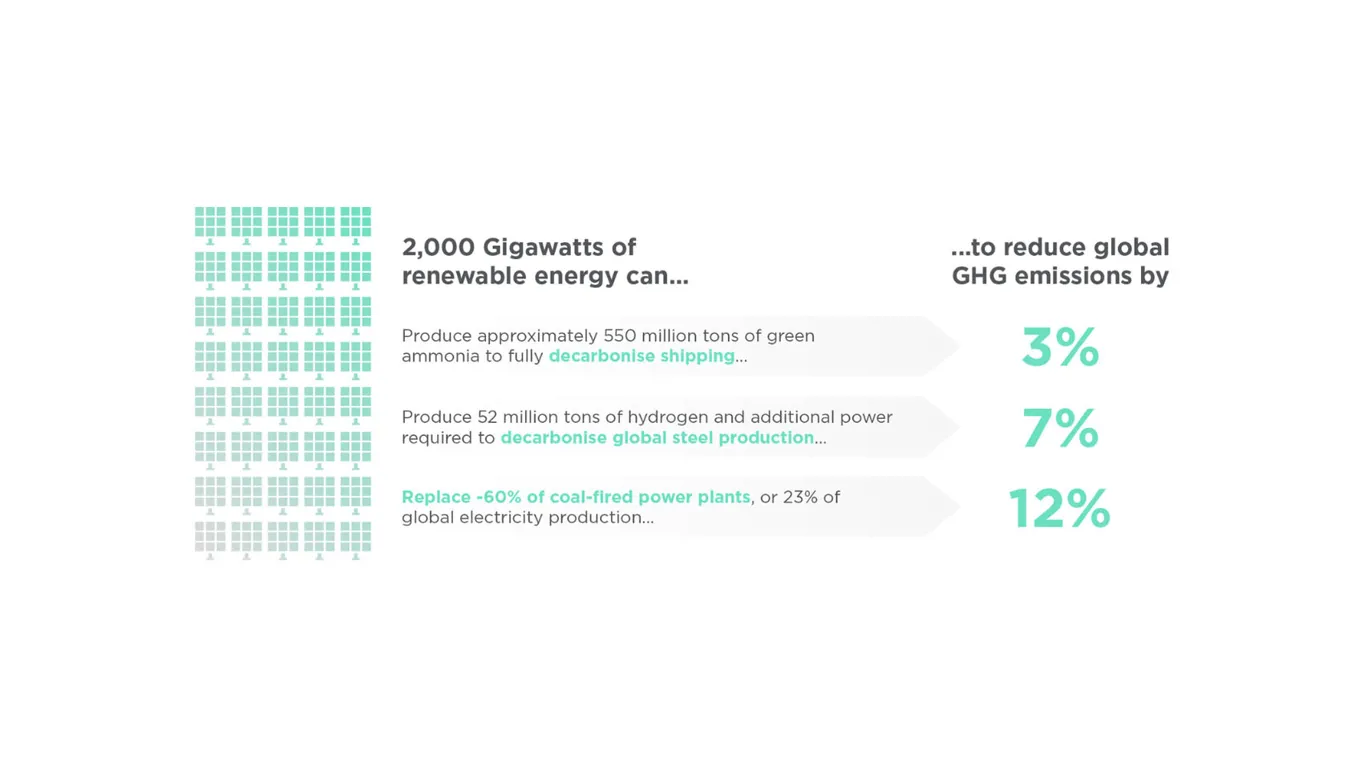

Achieving the complete transition of the maritime industry to e-fuels such as ammonia and methanol would require ~2,000 Gigawatts of renewable energy. This is a mammoth amount, and not the most sustainable use of resource when we consider that, if used in other industries, such as coal, the impact of the same resource in cutting global GHG emissions by 12% rather than 3% represented by shipping.

LNG is cleaner and more readily available than other fuels

Transition fuels such as LNG, although carbon-based, have a leading role to play as we work to achieve a zero-carbon future. In the short term, LNG can significantly reduce emissions as a sole substitute for conventional fuels and could cut the industry’s emissions by ~20% effective immediately full life cycle according to FuelEU – the most rigid maritime fuel regulation.

Unfortunately, LNG is somewhat controversial mostly thanks to a view voiced by certain members of academia and echoed by the World Bank - that emission reduction will be significantly smaller if you choose antiquated equipment and maximise methane slips throughout the value chain. This view fails to recognise that emissions are accumulative and any reduction small or large is better than nothing. Further on, methane slip from combustion is now almost negligible with the right engine technology and onshore emissions are currently being hit with heavy regulations.

In the medium term, we can look to further increase the positive impact of switching to LNG by blending with bio-LNG, which will enable us to reduce our emissions as an industry even further. The final solution is synthetic LNG, an e-fuel based on the same principles as e-methanol and e-ammonia, where renewable electricity is the key feedstock.

In summary, we fully support the progress the industry is making in the sphere of alternative fuels, as it lays the foundation for a future decarbonised shipping industry.

Without the methanol-capable ships in the orderbook, the relentless research and work towards making ammonia engines safe and viable, and the investments in electro-fuel production dedicated for shipping, the foreseeable future would look fossil. The key message is that while alternative fuels at scale is certainly a solution for the future, the ‘transition window’ of our next decade – when it is imperative that meaningful action is taken – calls for other solutions.

We should not allow our industry to be bound by box-ticking exercises for appearance’s sake to achieve our own industry goals to the detriment of a greener future. We need to effect sustainable change now – through the widespread use and investment into transitional fuels like LNG. While alternative fuels might be the right choice for specific projects today, they are not mature as a large scale solution for our industry in the near future.

Regulations should not be based on ideals and must instead be secured in reality and consider what is the best deployment of renewable energy resources for global benefit. Maritime is a leading industry in terms of technology and innovation, and we are not afraid of thinking outside of the box to lead the way. We do however ask that we are guided on a sustainable path towards decarbonisation and that we recognise the best options at hand.

Clarksons Green Transition Team

We are committed to helping our clients navigate a transitioning industry. Our Green Transition team can help you understand regulations, fuels and technologies, market impact and opportunities.

We work closely with all our business segments (ship broking, chartering, research, port services and investment banking) to provide a unique blend of tailored advisory services, from impact analysis to strategic development, right through to execution.

Clarksons wholly recognises that climate change is one of the biggest challenges of our time, and we all have a contribution to make. That’s why we strive to be a greener company by enabling global trade and leading positive change in the industry.