Ship design for CO₂ carriage is evolving rapidly with yards exploring various ship sizes and different pressure/temperature capabilities. While only a handful of small vessels have been ordered to date, there are strong indications that demand for CO₂ carriage will grow. Interest in the sector during Q2-2022 has outstripped even our expectations, but this interest is creating exaggerated demand, leading to confusion and price inflation. In this article we examine recent market movements for liquid CO₂ carriage and look ahead at what we might expect as the market matures.

Can we expect CO₂ carriage to grow significantly?

Yes, given the current drive to reduce CO₂ emissions, this is likely.

Will many more CO₂ carriers be contracted?

Almost certainly. What is less certain however is the number, size and design of these vessels as this will depend on firm projects being realised. The diversity of size/design requirements for CO₂ carriage and the costs involved means speculative orders are unlikely. Instead, we anticipate vessels being ordered against firm, long-term projects.

What is the current market situation?

Carbon Capture and Storage (CCS) with a shipping element, is still at an evolutionary stage. The impetus comes from industrial companies, often driven by engineering and upstream divisions. Shipping strategy has not evolved in the same way it has in established liquid gas trades, resulting in a number of unknown factors and a lack of experience. For the time being, the market may continue to be confusing and unstructured despite the significant investments being contemplated.

What is the solution to this?

Over time yards will gain experience as to how best to field CO₂ enquiries. It seems likely that initially, only a small percentage of enquiries may result in orders with significant wasted resources. In time however, the industry will be better understood and become more efficient. For now, yards may be reticent to engage in CO₂ carrier enquiries compared to their willingness to handle those for more established gas ship designs.

What is currently happening with CO₂ vessel design?

Virtually all the major shipyards in China, South Korea and Japan are working on CO₂ vessel designs. These range from 4,500 CBM right up to 70,000 CBM capacity and are at various stages of advancement. Clarksons is closely following the evolution of design specifications and prices. Please contact us if you’d like to hear more.

What CO₂ vessels have been ordered?

Over the last few months the number of enquiries has increased significantly, particularly in the range of 12-20,000 CBM. Several projects have been announced, which are at various stages of discussion, however only two firm orders have reportedly been placed to date, namely:

|

ORDER 1:

1,450 CBM CO₂ carrier by Sanyu Kisen Co.

|

|

Quantity

|

1

|

|

Shipbuilder

|

MHI Shimonoseki

|

|

Details

|

- Described as a ‘demonstration test ship’

- Part of the NEDO (New Energy and Industrial Technology Development Organization) project initiatives

|

|

Delivery date

|

Second half of 2024

|

|

Charterer

|

The Engineering Advancement Association of Japan (ENAA)

|

|

Operator

|

The Engineering Advancement Association of Japan (ENAA)

|

|

Price

|

No price has been reported

|

|

ORDER 2:

7,500 cbm CO₂ carrier by Northern Lights (JV Equinor, Shell & TotalEnergies)

|

|

Quantity

|

2

|

|

Shipbuilder

|

Dalian Shipbuilding Industry Co (DISC)

|

|

Details

|

- Required to withstand -80°C temperatures and 20 bar pressure (compared to 6-8 bar for a standard semi-ref gas carrier)

- Temperature/pressure requirements mean the actual material of the cargo tanks is still under development

|

|

Delivery date

|

Expected by mid-2024

|

|

Price

|

Reported to be in the region of US$ 51m each*

* This is an ‘open’, ‘research style’ project where additional costs may be incurred due to uncertainties on the design (including the material of the cargo tanks)

|

Where is the demand coming from?

Q2-2022 has seen a surge in demand. To our knowledge, the number of firm projects has not grown since February of this year so where has this increased attention come from? Northern Lights Phase 1 already has two vessels on order at Dalian, however Northern Lights Phase 2 invites CO₂ emitters to place their CO₂ within an expanded sequestration facility in Norway. It is this which we believe is creating at least some of the additional enquiries.

Why does an individual project create so much perceived demand?

CO₂ trade starts with the receiving sites, the Northern Lights terminal in Norway being a prime example. Sites like these (or at least those ready to receive CO₂ in the near future) are limited. Far less limited are the potential loading sites within Northwest Europe which could vie to place their emissions to Northern Lights (and other sequestration sites going forward).

Most loading sites are intended to be collection hubs for multiple industrial emitters. Given the significant investments required in order to capture, liquefy, collect and store the CO₂ at the loading port, emitters tend to work together in joint initiatives. This makes sense given the logistical and technical challenges of bringing emissions from several industrial points into one place for loading on ships, at scale.

Let’s take, for example, a single sequestration site, which has limited capacity to receive CO₂ shipments. It is used by many emitters from various locations around Europe which, together, are capable of fulfilling the sequestration capacity many times over. Consider that each of these emitters is making shipping enquiries with multiple prospective shipowners and you begin to see how a single sequestration project which could only realistically utilise around four ships, could be generating enquiries for up to forty ships.

Why is that a problem?

Multiple yards in Japan, Korea and China have done significant work on CO₂ ship design, encouraged by several owners who are interested in being ‘first movers’ in the sector. However, the designs vary significantly in terms of capacity and cargo technology (including pressure and temperature).

Yards are understandably looking to protect their designs by only releasing them under a signed NDA against named projects. For specific sizes of vessels, there may only be three or four yards with designs which are advanced enough to take orders within specific time frames.

The problem arises when those yards receive multiple enquiries from different buyers which originate from the same project, far outstripping the underlying requirement. This can create confusion with the artificial demand leading to upward pressure on pricing. It can also stifle the yard’s appetite to advance the existing design.

Is that happening already?

Yes, from what we understand, there are already many firm enquiries with the yards so we do therefore appear to be at that stage.

What has been the response from yards and how can Clarksons help?

Yards are likely to engage their (limited) design capability with those owners who have the most compelling story and/or those with whom they have a strong track record on other sectors. This is where Clarksons can help. Our long-standing experience and involvement with yards enables us to connect the appropriate stakeholders together on a project-by-project basis, preventing unnecessary noise

and avoiding inflated demand.

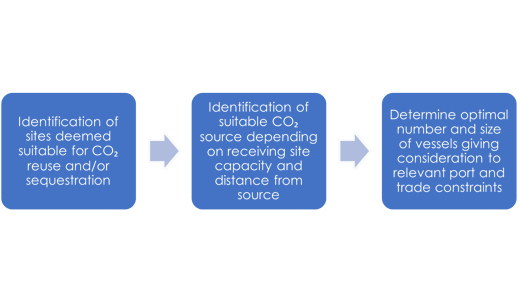

What will the trade look like 10 years from now?

As you may imagine, this is difficult to predict but trade evolution is likely to follow a pattern similar to the below:

Skip to main content

Skip to main content