Skip to main content

Skip to main content

LNG Shipping: Short-Term Headwinds, Long-Term Growth

In this week’s Analysis, we profile an LNG shipping market experiencing short-term headwinds (“spot” day rates hit record lows in early 2025 and remain well below trend) while anticipating a significant expansion phase (we expect trade volumes to grow 60% by the end of the decade). Not for the first time, it seems a case of ships delivering on time while projects have slipped back.

Not For The First Time...

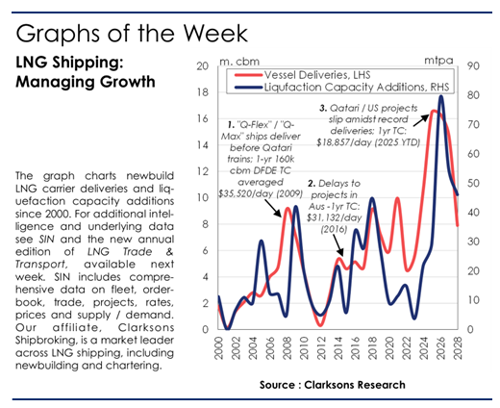

For the ~20% of LNG carriers trading on the short-term charter market, the past twelve months have seen some pretty “tough” conditions (a 1 year TC low of $9,000/day for a DFDE, steam turbine rates fell into negative territory). While recent trends in distance have not helped (most US exports have headed to Europe not Asia this year), projected fleet growth of 17% across 2024-25 set against volume growth of 7% over the same period highlight the currently weak “fundamentals”. With the scale of LNG trade expansion expected (2030 (f): 650mt, 2024: 412mt), judging the specific timing of shipping requirements (451 ships >40k cbm of $103bn ordered this decade) was always going to be “tricky”, particularly with the generally good record of shipyard delivery and a tendency for projects to “slip” (e.g. Golden Pass, North Field Expansion). As our graph shows, there have been previous parallels, albeit while managing smaller magnitude volume growth phases and without a material fleet renewal requirement (220 steam turbines, today 25% of fleet). And of course the majority of the LNG fleet (and orderbook) are committed on dedicated long term charters.

Volumes Set To Surge...

LNG trade volumes are now set for significant growth, with 2026 projections suggesting record expansion (80mtpa nameplate capacity onstream, >75% previous high). The project pipeline remains strong, with 140mtpa of capacity under construction and set to start-up in 2027-30 while up to 100mpta of capacity could reach FID this year (75mtpa in the US following 2024 delays). LNG trade is forecast to surge ~60% by 2030 amidst US (+100mt) and Qatar (+63mt) export growth. On a macro level, natural gas will be 23% of global energy supply by 2030 and should do well in the energy transition (but keep an eye on Chinese demand, geo-politics and gas pricing).

Fleet Expansion...

To support upcoming volumes, the LNG newbuilding orderbook (at 44% of fleet, 2025 forecast to be a record delivery year) is the largest in shipping. Ordering “paused” in 1H 2025 (only 8 orders) but there are still significant project requirements to support new orders in the next 18 months. South Korea (66% of orderbook) remains the market leader, with WinGD having the most popular engine and GTT dominating containment systems. Newbuilding prices are down 4% y-o-y. Our data suggests that ~65% of the fleet / orderbook is now owned by “independents”. And by end 2026, we project that the LNG fleet will be bigger than the VLCC fleet. Outside of mainstream LNG carriers, there have been 30 orders for LNG bunker tankers in the past 18 months and with 1,448 vessels in the fleet / on order LNG fuel capable (exc. LNG carriers) these assets will play a critical infrastructure role for the fuelling transition. So (perhaps understandably given the scale of potential expansion, fleet renewal and small spot market), LNG shipping is dealing with difficult issues of timing. But don’t forget what is (hopefully) around the corner!

The author of this feature article is Stephen Gordon. Any views or opinions presented are solely those of the author and do not necessarily represent those of the Clarksons group.

The graph charts newbuild LNG carrier deliveries and liquefaction capacity additions since 2000. For additional intelligence and underlying data see SIN and the new annual edition of LNG Trade & Transport, available next week. SIN includes comprehensive data on fleet, orderbook, trade, projects, rates, prices and supply / demand. Our affiliate, Clarksons Shipbroking, is a market leader across LNG shipping, including newbuilding and chartering.

About Clarksons Research

Clarksons Research, the data and analytics arm of Clarksons, are market leaders in the provision of independent data and intelligence around shipping, trade, offshore and the maritime energy transition. Millions of data points are processed and analysed each day to provide trusted and insightful intelligence to thousands of stakeholders across maritime. Better data for better decisions.