Skip to main content

Skip to main content

No Time to Waste: Clarksons Calls for Immediate Action on LCO₂ Shipping Post-NZIA

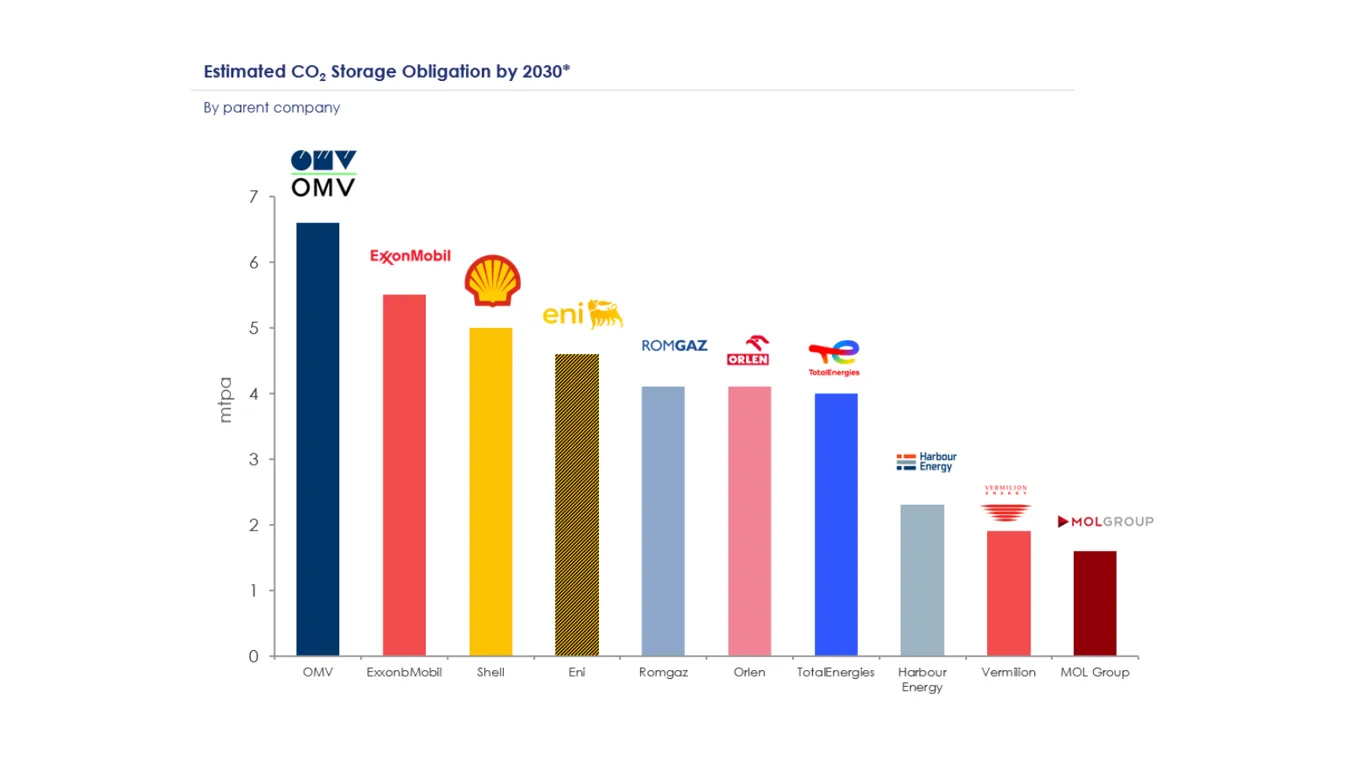

In a landmark move to accelerate industrial decarbonisation, the European Commission has enacted a pivotal decision under Article 23 of the Net-Zero Industry Act (NZIA). This assigns binding CO₂ storage obligations to 44 oil and gas producers across the European Union. The bloc must facilitate at least 50 million tonnes of annual CO₂ injection capacity into geological storage sites by 2030. By 2040 the EU Commission estimates the need to ramp up to 250 million tonnes.

The decision is still under a scrutiny period by Parliament and Council, but it directly links fossil fuel extraction to carbon storage responsibilities, and it underscores the urgent need to expand the LCO₂ shipping market in Europe.

The companies must submit a detailed plan on how they intend to meet their obligations by 30th June 2025. Given that many of the companies listed are not currently active in the CCS space, this presents a tight deadline for some actors. As a result, we are likely to see a variety of new collaboration structures emerge, as it is an opening to form agreements with third-party storage developers.

This is a clear signal that the EU is putting CCS at the top of the decarbonisation agenda, and the Oil & Gas producers in Europe will be forced to provide storage solutions for CO2 and help drive the value chain forward. No time to waste.

Kenneth Tveter, Global Head of Green Transition and LCO2 at Clarksons

The details of the directive must be explored, and there are unresolved aspects which require clarification such as penalties for non-compliance and the current exclusion of countries with advanced storage development (e.g., Norway and the UK). However, this move by the EU is a strong signal for the CCS industry in Europe. It places responsibility on oil and gas producers to act. This could increase competition for CO₂ storage, as many emitters are now forced to consider the very limited number of storage projects that have reached Final Investment Decision (FID).

Currently, the only alternatives in Europe are Northern Lights and Project Greensand. Providing emitters with more options to dispose of their CO₂ strengthens their negotiating position, potentially driving down costs, sharing risk, and ultimately enabling more projects to materialise. This is particularly significant for emitters not located near storage sites. However, it is important to remember that subsidies and regulatory incentives remain essential to fund capture projects, as CO₂ is a commodity with virtually negative value.

The NZIA leaves CO₂ transportation infrastructure out of scope, which represents a major bottleneck for emitters seeking access to storage. CCS value chains are complex infrastructure projects that typically take years to develop, with past projects indicating a 6–8 years timeline to reach operations. Given that we are now only five years away from the 2030 target, this is a critical concern.

“For many projects, shipping will be the only realistic transportation option to connect emission sources with storage sinks. It offers shorter lead times than pipelines, greater flexibility and scalability, simpler permitting processes, and in many cases, better economic efficiency” says Kenneth Tveter.

However, LCO₂ shipping is still an emerging market, with few vessels currently in operation or under construction—most of which are already committed for the next 10 to 15 years. This makes the construction of new vessels essential. Yet, there are no off-the-shelf solutions available, and solutions need to be tailor made for projects. While many shipowners are eager to enter the LCO₂ space, few are willing to order vessels without long-term contracts in place.

LCO2 carrier newbuild projects can be a complicated process and the vessel needs to be suitable for the value chain strategy. Initiating this process immediately is crucial, as vessel construction alone takes 2–3 years. This is in addition to time-consuming phases such as FEED, vessel design, and various negotiations.

The shipbuilding market is complex and the yards appetite and capability to build LCO2 carriers is dynamic and market dependent. Executing newbuilds requires unique yard competence and commercial and technical knowledge. If you are not working on your LCO2 shipping strategy today, including project execution plans, you’re already behind.

Projects that delay these steps will fall to the back of the queue, and shipyard capacity is limited. In other words, any project aiming to store or dispose of CO₂ by 2030—and not located next to a suitable storage site—must begin developing its LCO₂ shipping strategy today.

Clarksons Green Transition and LCO2 team are ready to help.